Tax management has grown more complicated than ever! Whether it’s tax changes, compliance guidelines, or more stringent financial reporting, businesses have to ensure that all their tax-related processes are conducted with accuracy. There could be penalties, audits, reputation or financial loss due to even a minor mistake. In-House vs Outsourced Tax Services.

This raises an important question for growing businesses:

Should you have in-house tax staff or hire experienced tax pros to outsource tax services?

Not everything is clear cut. An internal tax team allows for more control and direct oversight, but an outsourced team can offer increased expertise, reduced operational costs, cutting-edge technology, and scalability options that many businesses may not be able to replicate.

From a startup to an SME, accounting firm, CPA practice to large enterprise, the right tax management strategy can have an immediate effect on profitability, compliance, efficiency, and long-term growth.

Here’s a comprehensive guide to comparing in-house and outsourced tax services, exploring the pros and cons of both, contrasting costs, and deciding which option is more suitable for your firm’s needs.

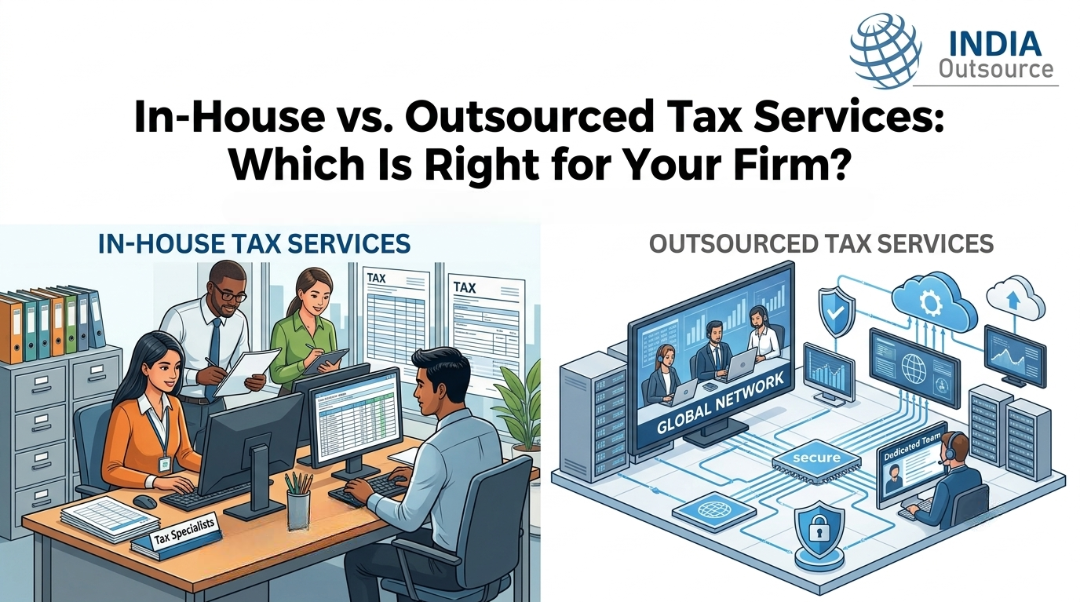

What Are In-House Tax Services?

In-house tax services include having full-time staff in your office to handle your tax needs.

A typical internal tax department may include:

- Tax Managers

- Tax Accountants

- Financial Controllers

- Compliance Specialists

- Payroll Tax Experts

- Tax Analysts

These experts are your employees only and handle all of the tax planning, filing, reporting, audit and regulatory compliance for your business.

Responsibilities of an In-House Tax Team

An internal tax department usually manages:

- Corporate tax preparation

- Sales tax compliance

- Payroll tax reporting

- GST/VAT compliance

- Tax planning strategies

- Financial reporting

- Tax audits

- Regulatory compliance

- Internal documentation

- Risk management

The company has the responsibility of recruiting, training, managing and retaining these professionals.

What Are Outsourced Tax Services?

Outsourced tax services are based on a third party accounting/tax service working on your tax obligations.

Rather than having a large in-house tax team, businesses partnering with an experienced tax team of remote workers who use cloud-based accounting software that is secure.

These firms often provide:

- Tax preparation

- Tax filing

- Bookkeeping

- Payroll processing

- Corporate tax planning

- Sales tax management

- Audit support

- Financial reporting

- CFO advisory services

- International tax compliance

Outsourcing is a flexible and budget-friendly option for businesses, as they only pay for the services they need.

In-House vs. Outsourced Tax Services: Quick Comparison

| Feature | In-House Tax Team | Outsourced Tax Services |

| Cost | High | Lower |

| Hiring Required | Yes | No |

| Employee Benefits | Required | Not Required |

| Training Costs | High | None |

| Compliance Expertise | Limited | Extensive |

| Scalability | Difficult | Easy |

| Technology Investment | Required | Included |

| Availability | Business Hours | Often Extended Support |

| Risk Management | Internal Responsibility | Shared with Experts |

| Access to Specialists | Limited | Broad Expertise |

| Business Focus | Administrative Burden | Focus on Growth |

Advantages of In-House Tax Services

1. Greater Control

Internal employees are those that are working within your organization, and your management can keep a close watch on the tax processes.

This kind of control is useful for companies that have specific functions or delicate financial details.

2. Immediate Communication

The tax team is on-site or part of your structure, which means that communication is more effective and rapid.

Managers can easily discuss tax strategies, financial planning, immediate compliance issues, etc. without having to coordinate with an outside provider.

3. Better Understanding of Company Operations

Internal employees learn a lot about you’re:

- Business model

- Financial structure

- Revenue streams

- Industry regulations

- Internal workflows

This knowledge can be helpful when making decisions on tax planning for the company.

4. Dedicated Resources

An in-house tax department works solely for your company, whereas outsourced tax departments work for several firms.

This focused effort can be of great value to businesses with especially complex tax situations.

Disadvantages of In-House Tax Services

High Operational Costs

The internal tax department can be very costly.

Costs include:

- Salaries

- Bonuses

- Health insurance

- Retirement benefits

- Office space

- Recruitment

- Software licenses

- Hardware

- Employee training

These expenses can be a burden for many businesses.

Recruitment Challenges

It’s harder to find professionals with experience in taxation.

Businesses may invest months in finding qualified candidates but still have to deal with larger businesses paying higher salary.

Limited Expertise

A single inside team might not have an in-depth understanding of:

- International taxation

- Multi-state compliance

- Industry-specific tax laws

- Mergers and acquisitions

- Cross-border tax planning

But complex issues could still call for outside consultants.

Continuous Training Requirements

Tax regulations constantly changing.

Businesses must invest in ongoing employee education to remain compliant with changing legislation.

Advantages of Outsourced Tax Services

Significant Cost Savings

Cost reduction is one of the most important reasons that companies outsource their tax services.

Businesses eliminate expenses related to:

- Recruitment

- Employee salaries

- Benefits

- Office infrastructure

- Software purchases

- Professional training

Rather, they only pay for the services they require.

Access to Experienced Tax Professionals

Outsourced providers have a group of experts working in a variety of industries and jurisdictions.

This means your business benefits from:

- Senior tax advisors

- CPAs

- Compliance experts

- Audit specialists

- Payroll professionals

- International tax consultants

Without employing each one separately.

Better Compliance

Specialist tax companies keep up to date on ever-evolving tax legislation.

They proactively monitor:

- Legislative changes

- Filing deadlines

- Compliance requirements

- Reporting standards

This greatly reduce the danger of penalties and audits.

Scalability

Business needs change over time.

When you’re looking to expand your business into new markets, buy another business, or during tax season, you can add services without needing to hire more people, outsourced providers can simply scale it up.

Advanced Technology

The vast majority of outsourcers will be working with cutting-edge cloud accounting solutions and automation.

Benefits include:

- Secure document sharing

- Real-time reporting

- Automated workflows

- Digital tax filing

- Data backups

- Improved accuracy

You can benefit from enterprise-level tech without the enterprise price tag.

Improved Business Focus

Compliance with the tax law takes up significant management time.

Outsourcing allows business leaders to focus on:

- Growth

- Customer acquisition

- Product development

- Sales

- Strategic planning

Rather than administrative duties.

Disadvantages of Outsourced Tax Services

Less Direct Control

For some business owners, it’s preferable to oversee tax things themselves.

It may be necessary to set up communication and reporting with an external provider.

Initial Transition

Transferring financial data to a different provider may take some time.

But, when a business is an expert in outsourcing, they usually have a detailed procedure for getting new hires up and running that lessens the chaos.

Data Security Concerns

This is a concern that many businesses have when it comes to sharing a part of their finances that is sensitive.

A good outsourcing company will handle this by:

- Encrypted systems

- Secure cloud platforms

- Multi-factor authentication

- Confidentiality agreements

- Regulatory compliance

- Regular cybersecurity audits

Cost Comparison

In-House Costs

Typical expenses include:

- Employee salaries

- Payroll taxes

- Benefits

- Recruitment fees

- Software subscriptions

- Office equipment

- Training programs

- Management overhead

These reoccurring costs can be significant, particularly for small and mid-size businesses.

Outsourcing Costs

Businesses generally pay:

- Monthly service packages

- Project-based pricing

- Hourly consulting fees

- Seasonal tax preparation costs

But, on average, outsourcing can offer substantial benefits from a cost-cutting standpoint, as well as access to more extensive expertise.

Which Businesses Should Choose In-House Tax Services?

If your business: An internal tax department might be needed if you:

- Has thousands of employees

- Operates in highly regulated industries

- Requires daily tax decision-making

- Has complex multinational operations

- Can support the high costs of maintaining a dedicated tax department

Which Businesses Benefit Most from Outsourced Tax Services?

Outsourcing is ideal for:

- Startups

- Small businesses

- Mid-sized companies

- CPA firms

- Accounting firms

- E-commerce businesses

- Healthcare organizations

- Manufacturing companies

- Law firms

- Real estate businesses

- Non-profit organizations

These companies can enjoy the advantages of specialized expertise without the expense of a dedicated tax department.

Key Factors to Consider Before Making Your Decision

When deciding on one of the two options, in-house or outsourced tax, consider the following:

Business Size

Outsourcing might be more beneficial for smaller companies, whereas larger businesses may need their own teams.

Budget

Before making a decision, work out the actual expenses of hiring, training, benefits, software and infrastructure.

Complexity

International businesses or those operating in multiple countries will likely need a particular level of tax expertise, which outsourcing providers can provide.

Growth Plans

Growing businesses require flexibility in their tax structure that can grow with them without significant recruitment.

Technology Requirements

Decide whether your company is ready to invest in cutting-edge accounting software and secure tax management systems.

Hybrid Approach: The Best of Both Worlds

What many businesses do is to have a small finance team internally and outsource specialized tax services.

This approach offers:

- Internal oversight

- External expertise

- Lower operational costs

- Better compliance

- Greater flexibility

- Access to specialized advisors when needed

It is becoming a very common method among expanding enterprises to manage and be efficient.

Conclusion: Which Option Is Right for Your Firm?

When it comes to choosing between in-house and outsourced tax services, there’s no one right or wrong answer. It’s up to you to choose the right one depending on your business size, budget, operational complexity, compliance requirements and long-term goals.

For those that want to have full control, and can support a dedicated tax function, an in-house tax team might be the best choice. For many small to medium-sized businesses, outsourcing offers even more value as a way to save money, gain specialized expertise, ensure compliance, leverage advanced technology, and scale with the business.

The bottom line is that you’re not just cutting costs—you’re creating a tax management strategy that helps your business grow sustainably, reduce risk and let your team focus on doing what they do best: growing your business.

Ready to Simplify Your Tax Management?

Contact Us Today

FAQs

- What is the difference between in-house and outsourced tax services?

In-house tax services are handled by full-time employees within a company, while outsourced tax services are managed by an external accounting or tax firm. Outsourcing provides access to specialized expertise, lower operational costs, and greater scalability, whereas in-house teams offer more direct control over tax processes.

- Is outsourcing tax services more cost-effective?

Yes. Often, outsourcing tax services will cost less since the business does not incur the cost of hiring staff, salaries, employee benefits, office space, software, etc., and there is no need to train employees. Only those services that are needed are paid for by companies.

- Which businesses should outsource tax services?

The benefits of outsourced tax services are most advantageous for small businesses, startups, CPA or accounting firms, ecommerce businesses, healthcare organizations, manufacturers and growing businesses, as they offer lower costs, expert support and are also more scalable.

- Are outsourced tax services secure?

Yes. Reputable tax service providers use encrypted cloud platforms, secure file-sharing systems, multi-factor authentication, and strict confidentiality policies to protect sensitive financial and tax information.

- Can outsourced tax professionals handle tax audits?

Absolutely. Numerous outsourced tax agencies offer audit preparation, documentation, representation with tax authorities, tax compliance reviews, and audit support after audit services to assist businesses in managing tax audits effectively.

- What are the advantages of an in-house tax team?

An in-house tax team provides more control over financial operations, speedy internal communication, better understanding of company operations and support in dealing with complex day-to-day tax issues.

- What are the benefits of outsourcing tax services?

Outsourcing provides access to experienced tax professionals, reduces operational costs, improves tax compliance, minimizes filing errors, offers advanced technology, and allows businesses to focus on core operations.

- How do I choose between in-house and outsourced tax services?

Consider factors such as your business size, budget, tax complexity, compliance requirements, growth plans, and available internal resources. Smaller and growing businesses often benefit more from outsourcing, while large enterprises may prefer maintaining an in-house tax department.